TOPICS

Zac Maymin & Mark Weisenborn

Supervisory Guidance

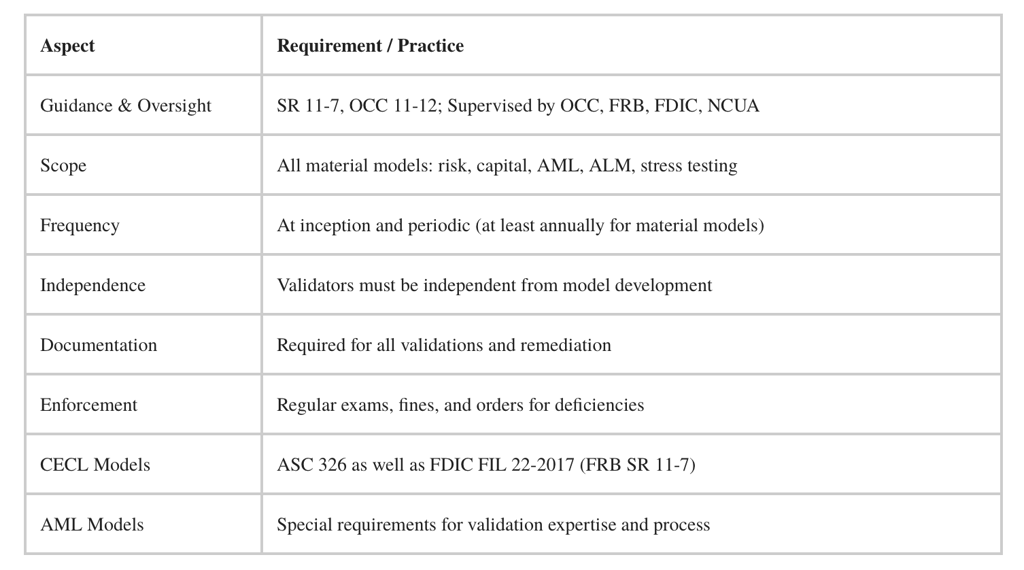

The cornerstone of model validation regulation in the U.S. remains the Supervisory Guidance on Model Risk Management (SR 11-7), originally issued by the Federal Reserve and the OCC, and later adopted by the FDIC. It requires banks to establish comprehensive frameworks for model risk management, including initial and periodic model validation.

Regulatory Agencies

Oversight is led by federal agencies such as the OCC, FRB, FDIC, and NCUA. These bodies outline validation standards, conduct examinations, and issue enforcement actions for non-compliance or deficiencies.

Frequency

Models must be independently validated at inception and periodically—at least annually or more often for higher-risk models.

Independence

Validators must be organizationally independent from model development teams to ensure unbiased assessments.

Scope

Validation covers all material models, including those for credit risk, capital adequacy (stress testing), anti-money laundering (AML/BSA), asset/liability management, and more.

Process Components

Comprehensive validation includes reviewing conceptual soundness, data integrity, model performance (outcome analysis), proper implementation, and ongoing monitoring.

Documentation

All validation activities, findings, and remediation actions must be clearly documented and subject to internal audit.

Expanding Focus

Regulation now applies to banks of all sizes, not just large institutions, especially for critical models such as those used for AML compliance.

Enforcement

Failures in model validation have resulted in significant enforcement actions and fines, with regulators demanding prompt remediation. Regulators may inquire on the qualifications of validators, including the technical background and ability to test system implementation.

Ongoing Updates

Regulatory agencies continually update guidance and expectations, with 2025 seeing an emphasis on governance, independent review, and validation transparency.

Stress Testing

For large banks, the Federal Reserve's annual stress tests use independently validated supervisory models. The process is overseen by dedicated model validation groups and an external Model Validation Council of academic experts.

AML Models

OCC 11-12 guidance requires banks to validate both internally developed and vendor AML models. Validators must have expertise in money laundering and financial investigations, and proper model documentation is mandatory.